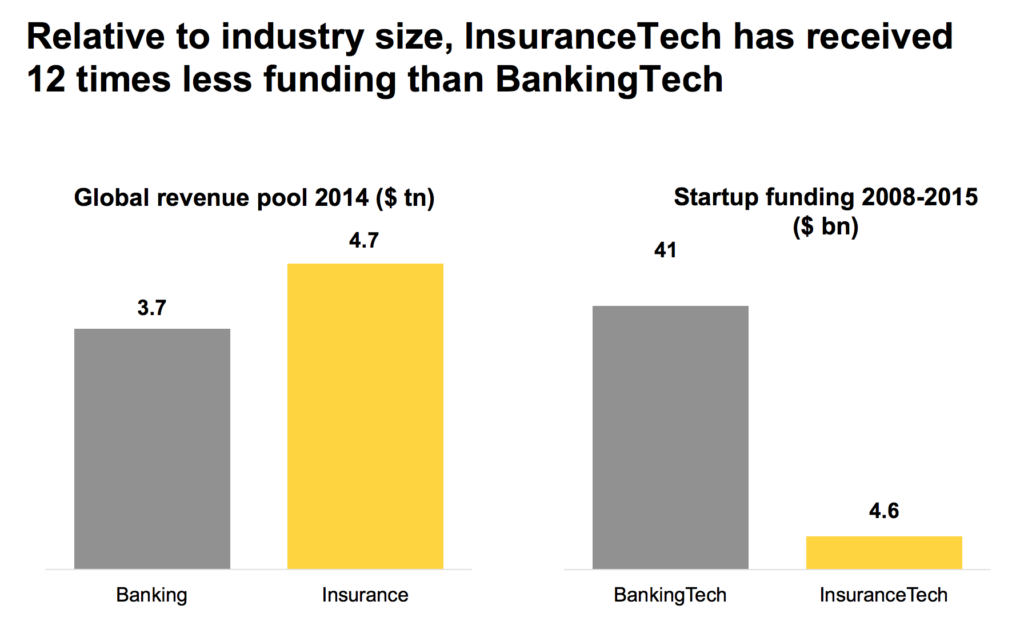

According to CommerzVentures – the venture capital fund of the German group Commerzbank – the insurance sector has received 12 times less funding between 2008 and 2015 than the financial sector, taking into account the insurance sector’s size based on 2014 figures.

This suggests there are still many opportunities left to exploit in the insurance sector, for both startups and well-established insurers who have spent years strengthening their profile in the market.

Robo-advisors are a tech innovation with great potential to occupy a large share of this growing and unchartered territory in the insurance sector. But how will they fit into the industry?

What is a robo-advisor?

A robo-advisor (alternative spelling “robo-adviser”) is an online platform that produces automated advice based on algorithms without the need for any human intervention.

According to the official definition by Investopedia, a robo-advisor is an “online wealth management service that provides automated, algorithm-based portfolio management advice without the use of human financial planners.”

How are robo-advisors related to AI?

“The power of artificial intelligence is based on large-scale data processing, algorithms and processing speed. The problem with any kind of analysis, investment and dispensing advice, either for investment or insurance products, is down to the limitations of human capacity.

– Ignacio Amiguet, CEO & Founder at Infinda

Artificial intelligence acts in exactly the same way as a human advisor – understanding customer needs, studying the market and giving the best possible advice – but in record time. The systems are automated to work perfectly, to be updated at all times, and in optimized versions, they actually respond to behavioral changes and adapt to new needs.The robo-advisor is capable of looking at all things at once, making all possible comparisons and optimization treatments, all in a matter of seconds. What seemed like something from the future is already the present.”

Robo-advisors are usually associated with Fintech or financial sector solutions since several similar products have cropped up in this industry, acting as online financial advisors whose spectrum of capabilities mainly fall within the category of wealth or asset management.

Source: Emerging Technologies Transforming the $4tn Insurance Industry by CommerzVentures

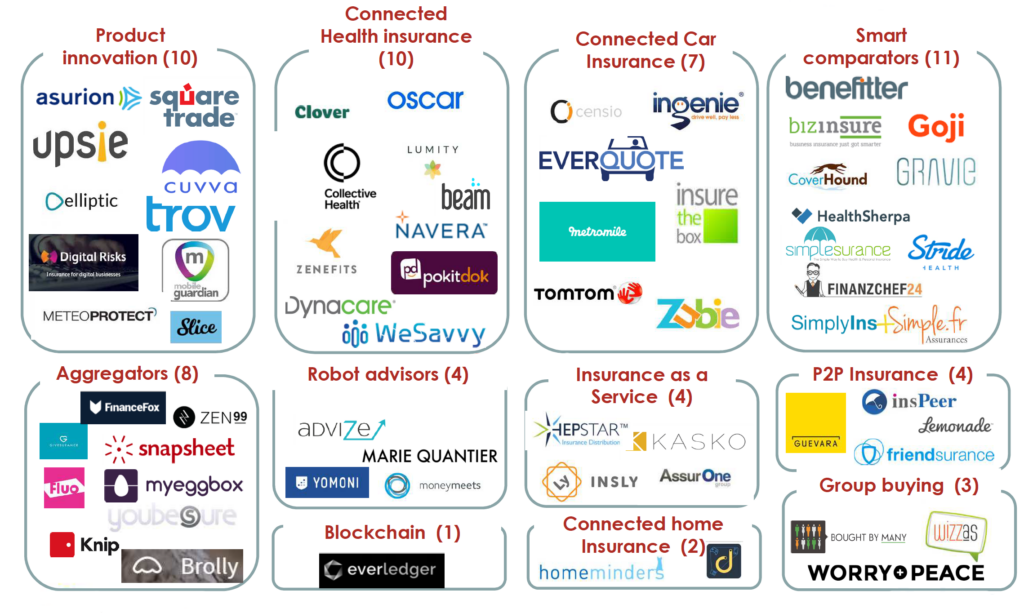

However, robo-advisors are also being used in the insurance sector, since those platforms that produce automated algorithmic recommendations are also suitable to recommend insurance products. New market players that have already been classified as robo-advisors include Yomoni, moneymeets, advize or Marie Quantier.

Simple, safe and transparent, these new technological innovations are in demand with new digital consumers who prefer making quick and efficient online purchases before reaching the point of needing personal assistance solutions.

This growing demand for solutions that are adapted for the needs of digital consumers is highlighted by Capgemini’s 2014 survey, in which only 29% of the insured parties are actually satisfied with their insurance providers.

To reverse this trend, insurers must prioritize customers’ needs and offer solutions that allow them to acquire and easily manage their insurance, taking advantage of their own data for obtaining the products that best fit their profile.

Therefore, robo-advisors or recommendations from automated platforms have an obvious relevance for insurers, since they act as complementary solutions to their direct and personal services.

Being customized management tools, robo-advisors will facilitate providing optimized customer experiences by choosing the products that best fit the customer needs, thanks to their high data processing capacity.

Source: From Connected Insurance as part of the Global Summit for Insurance Innovation event.

What role will robo-advisors play in the insurance sector?

Robo-advisors will play a crucial role in the not-too-distant future, for the following reasons:

- Unbiased advice: any advice from a robo-advisor is guaranteed to be absolutely objective. Any suspicion the client may have that the recommended product has been influenced by commissions or subjectivity is eliminated. A robo-advisor can also take into account multiple variables beyond price and process all of them to offer unbiased comparisons of superior products.

- Anticipation of needs: these artificial intelligence tools are able to process large amounts of data to predict and anticipate future needs in seconds. This helps customers to identify solutions best suited to their needs, budget and standards of quality.

- Strengthening the omnichannel strategy: with bots offering customers advice easily, quickly and around the clock, which is essential to provide a sense of closeness and availability to the digital customer, the use of robo-advisors will strengthen the integration of all channels of interaction that mediators or insurers may have with their clients.

Although it may seem counterintuitive, these tools will not replace insurance intermediaries as recommenders of products. They are programmed to interact with the user but do not replace personal contact and human interaction.

Since the human touch will remain a relevant part of any insurance transaction, robo-advisors serve to help strengthen the traditional relationship of trust that mediators and insurers have with their customers, since all conversations and meetings will be complemented by the automated platform.

Chances are that the exclusive use of a robo-advisor (in other words, without the intervention of a professional advisor) would only occur for basic insurance products that customers can take out themselves online without having to consult with advisors or insurance brokers.

Since hiring more complex products is a significant cost for companies and individuals, as well as depending on the intelligence of a robo-advisor, customers themselves will need the intervention of a trusted professional to help them understand all the information provided and purchase the insurance product that best suits their needs and preferences.

How should a robo-advisor be in the insurance sector?

The ideal automated advisor in the insurance sector should be capable of carrying out the following tasks:

Source: AI – The potential for Automated Advisory in the Insurance Industry by Surely Group & ACORD

- Capture and store: get basic information about clients and their existing policies, and store all data securely.

- Manage and analyze: manage all policies to know – among other things – when they need to be renewed so as to alert the insured party in time. Analyze the terms and conditions of each product in case there are others that offer the same or better coverage at a lower price.

- Advise and optimize: advise clients of policies to ensure their insurance portfolio is always optimized and best fits their needs and budget at all times.

- Contract, renew and cancel: provide the insured party the option to hire, renew or cancel policies if they are not suitable.

For a flawless customer journey, the electronic signature is a complementary tool to any automated counseling platform. Its easy integration via API makes it possible for these tools to not only provide advisory services, but also facilitate the recruitment or renewal of insurance policies without “forcing” the customer to switch platforms.Thus, insurtech robo-advisors can become a perfect digital medium to offer policyholders the ability to easily self-manage insurance policies, analyze its coverage and receive recommendations to optimize their portfolio, and sign new policies as well as cancel existing ones. And all this can be easily managed from a single app installed on your mobile phone.

How can insurers and insurance agents get the most out of robo-advisors?

According to Deloitte’s report Robo-Advisors – Capitalising on a Growing Opportunity, there are three main options for agents and insurance companies to gain the benefits offered by these automated platforms:

- Partnering with an existing robo-advisor.

This option enables the necessary technology quickly, easily and at a lower cost than the other two. - Acquiring a robo-advisor.

While the advantages of this option are similar to the previous one, its capacity for growth, its technological conditions and the robo-advisor’s potential fit within the company, especially in terms of digital culture, must be taken into account. - Developing an in-house solution.

This option is the least favorable in terms of cost and in terms of the necessary staff and knowledge needed to develop a good product internally.

RELATED POSTS